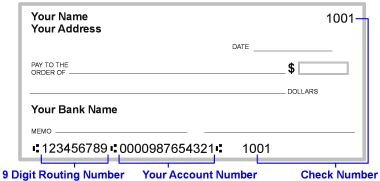

WHAT IS AN ABA ROUTING NUMBER?

American Bankers Association (ABA).

This number is always immediately to the left of the account number (or the “DDA Number”) at the bottom of every check that is issued in the US. The ABA (or routing number) is always 9 digits and is the unique identifier for the bank that issued the check.

International banks have similar numbers to code their checks. Many countries use “SWIFT” numbers.

WHAT IS AN ACQUIRING BANK?

This is also referred to as a “sponsor bank”, a “member bank” or simply an “acquirer”. The Acquiring Bank typically works through an “ISO” (Independent Sales Organization) to provide the business owner with a merchant account. Ultimately, when a credit card is run by a business owner, the acquirer accepts the payment for that business owner through the merchant account they have set up.

WHAT IS THE ACQUIRER PROCESSING FEE (APF)?

All VISA transactions in the US (if the transaction is “acquired” in the US) are subject to this 1.95¢ ($0.0195) fee (as of 12/2015). Any business based in the US will have the acquirer processing fee added to all of their Visa authorizations. This is the Visa equivalent to the MasterCard NABU fee.

WHAT IS AN ASSESSMENT FEE?

The Assessment fees are Visa and MasterCard’s primary revenue source.

You could look at this like a licensing fee, or a royalty that is paid to the Association (the brand of card) for every single transaction.

Visa and MasterCard each assess 0.1185% and 2¢ per transaction.

Discover also has an assessment fee: 0.10% and 2¢ per transaction.

Additional assessments apply to international cards and currency conversions, ranging between 0.4% – 0.8% above this and other fees.

Other notable fees:

In addition to assessments, VISA also charges an APF fee and MasterCard charges a NABU fee

Click Here to find All Visa Interchange Rates (2015 Visa Interchange Rates)

Click here to find All Mastercard Interchange Rates (2015 Mastercard Interchange Rates)

WHAT IS “THE ASSOCIATION”?

Though it’s singular, people are generally referring to both Visa & MasterCard when they use the term “The association”.

Technically, the association is the brand of the card you’re referencing. That could refer to the Visa Association, the MasterCard Association, Discover, American Express, JCB (Japanese Credit Bureau) etc. The associations’ role is generally to create the rules around using and accepting credit cards – as well as working with the card issuing banks to set the fee structure for each card (we call that fee structure “interchange”).

Each association charges business owners an “assessment fee” on every transaction processed. Sometimes this is very clearly stated on a merchant processing statement and sometimes it’s not listed at all. Typically with tiered pricing you will not see the assessment fee on a statement, but if you are priced with “interchange plus” pricing, the assessment fee will be listed as an individual line item. It is always assessed on all transactions world wide.

WHAT IS AN MCC CODE?

A Merchant Category Code is a four-digit code used to group all business in the world into different categories. This is an alternative to using “SIC codes” (Standard Industry Codes), which are used by other governing bodies. The Card Brands (Visa, Mastercard, AMEX, or Discover) assign these MCC codes a company when they are going to accept payments.

These numbers classify the business by the type of goods or services provided.

For business owners, the MCC assigned to their company can impact the cost of processing transactions, the level of risk banks associate with their company, or even the ability to accept payments from certain customers.

WHAT IS TIERED PRICING?

Tiered pricing is where the merchant account provider groups transactions based on certain “qualifications” and assigns a rate to each group or “tier.” These tiers are variable from one processor to the next prohibiting any direct comparison from a Tier 1 provided by one provider to a Tier 1 provided by another provider. For example, a basic tiered pricing would look like this:

- Qualified Discount Rate: x%

- Mid-Qualified Discount Rate: x.x%

- Non-Qualified Discount Rate: x.xx%

What is Interchange Plus Pricing?

Interchange plus pricing is based on two rates from the interchange tables, published by both Visa Interchange and MasterCard Interchange. This type of pricing creates a discount rate by adding interchange rates plus a percentage and authorization, or transaction, fees. This is a common pricing model for very low and very high average tickets as merchants pay a flat fee regardless of the processing rate.